Molded Fiber Lids and Cold-Drink Service Packaging Market Forecast 2026-2036: Global Market to Reach USD 3.1 Billion by 2036 at 9.08% CAGR

Molded fiber packaging is shifting from eco-trend to essential, driven by plastic bans, cost pressures, and demand for durable, compostable solutions.

Molded fiber packaging is shifting from eco-trend to essential, driven by plastic bans, cost pressures, and demand for durable, compostable solutions.

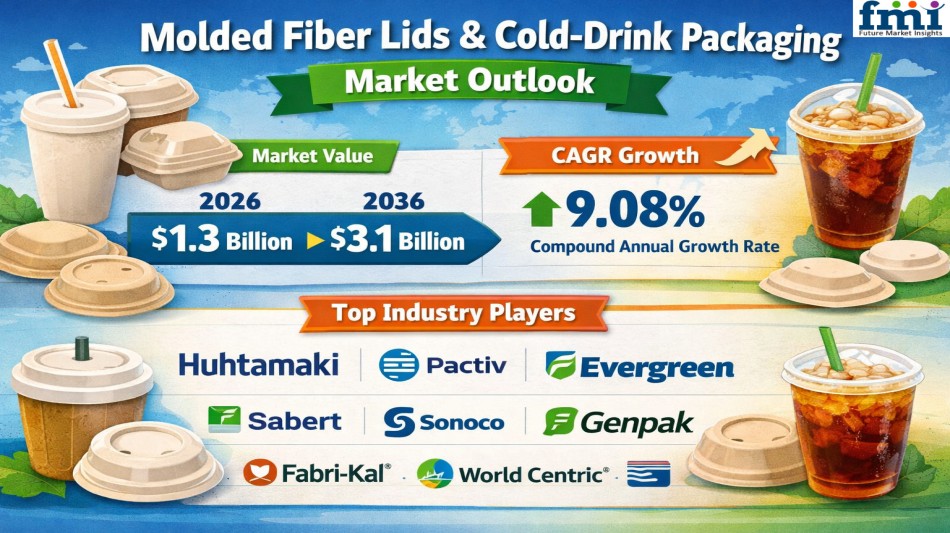

NEWARK, DE / ACCESS Newswire / March 17, 2026 / The global molded fiber lids and cold-drink service packaging market is entering a decisive decade of structural transformation, driven by tightening environmental regulations, evolving waste economics, and rapid material innovation. Valued at USD 1.3 billion in 2026, the market is forecast to reach USD 3.1 billion by 2036, expanding at a robust CAGR of 9.08%, according to a comprehensive analysis by Future Market Insights (FMI).

This growth reflects a fundamental shift across global foodservice ecosystems: molded fiber packaging is no longer a sustainability experiment but a mission-critical operational requirement. As municipalities aggressively phase out expanded polystyrene and impose punitive mixed-waste disposal fees, beverage chains and quick-service operators are accelerating their transition toward precision-engineered fiber solutions capable of matching plastic in durability, leak resistance, and performance under high-condensation conditions.

Market Metrics Snapshot

Metric

Value (2026-2036)

Market Size (2026)

USD 1.3 Billion

Forecast Value (2036)

USD 3.1 Billion

CAGR

9.08%

Top Growth Market

India (11.2% CAGR)

Leading Segment

Lids (45.2% Share)

Discover Growth Opportunities in the Market - Get Your Sample Report Now

https://www.futuremarketinsights.com/reports/sample/rep-gb-32326

The Structural Shift: From Plastic Dependency to Fiber Engineering

The molded fiber packaging industry is undergoing a material transformation as operators abandon legacy plastics in favor of high-performance, compostable alternatives. This shift is not incremental-it is systemic.

High-volume beverage chains are rapidly moving away from spot-market plastic procurement and entering multi-year fiber offtake agreements to secure supply continuity. Delaying this transition is proving costly, exposing operators to severe margin compression amid volatile raw material pricing and constrained tooling capacity.

At the same time, downstream waste economics-particularly in large venues such as stadiums and transit hubs-are increasingly dictating packaging decisions. The ability of fiber-based products to seamlessly integrate into municipal composting infrastructure is now a defining factor in procurement strategies.

The PFAS Barrier: The Industry's Defining Inflection Point

One of the most critical technological thresholds shaping the market is the elimination of per- and polyfluoroalkyl substances (PFAS). These chemicals, historically used for water resistance, are facing growing regulatory scrutiny worldwide.

The industry stands on the cusp of a breakthrough: once material scientists successfully commercialize bio-based, PFAS-free barrier coatings capable of withstanding prolonged exposure to condensation, a rapid and large-scale transition will follow. This innovation will unlock global procurement networks, enabling beverage chains to shift entire cold-drink portfolios to fiber-based solutions almost instantly.

Segment Spotlight: Lids, Bagasse, and QSR Dominance

Protective Fiber Lids Lead Adoption

Molded fiber lids are projected to capture 45.2% of the market share in 2026, emerging as the fastest pathway to regulatory compliance. Unlike cups, which require structural redesign, lids offer a targeted upgrade that delivers immediate environmental alignment with minimal operational disruption.

However, performance remains non-negotiable. Fiber lids must achieve precise snap-fit integrity to prevent leaks during high-speed drive-thru operations. Products that fail to meet these standards are quickly rejected, regardless of sustainability benefits.

Bagasse: The Backbone of Fiber Innovation

Bagasse, derived from sugarcane residue, is expected to hold 38.5% of the material share in 2026. Its long-fiber structure enables manufacturers to produce complex geometries and deep undercuts essential for secure lid fitment.

This material advantage significantly reduces production defects and ensures durability under cold, moisture-heavy conditions-making it the preferred feedstock for premium applications.

Quick Service Restaurants (QSRs): The Primary Demand Engine

The QSR segment dominates with a 52.1% market share in 2026, reflecting the sector's urgent need to replace plastic packaging. Despite cost sensitivities, QSR operators are compelled to adopt advanced fiber solutions to avoid regulatory penalties and operational disruptions.

Interestingly, while fiber packaging carries higher upfront costs, lifecycle economics often favor it due to savings from avoided landfill fees, EPR taxes, and compliance risks.

Regional Powerhouses: Asia-Pacific Leads the Acceleration

India (11.2% CAGR): The Fastest-Growing Market: India is projected to lead global growth with an 11.2% CAGR, fueled by strict federal bans on single-use plastics and the rapid expansion of organized foodservice chains. The country's strong domestic bagasse supply provides a strategic advantage, enabling localized production and cost efficiency.

China (10.5% CAGR): Manufacturing and Innovation Hub: China continues to dominate both production and innovation, leveraging its extensive pulp infrastructure to achieve price parity with plastics. Its advanced thermoforming capabilities are setting global benchmarks for production speed and efficiency.

Europe: Regulation-Driven Transformation: Countries like Germany (9.5% CAGR) and the United Kingdom (8.8% CAGR) are witnessing accelerated adoption due to stringent Extended Producer Responsibility (EPR) frameworks. These policies are transforming fiber packaging from a sustainability choice into a financial necessity.

United States (7.2% CAGR): Fragmented but Accelerating: In the U.S., a patchwork of local regulations is forcing national brands to standardize packaging at the highest compliance level. This trend is driving widespread adoption of molded fiber solutions across the country.

Market Dynamics: Tooling Bottlenecks and Supply Chain Realignment

Despite strong demand, the market faces a critical constraint: precision tooling capacity. Manufacturing high-performance fiber lids requires specialized molds with exact tolerances, and the lead time for developing such tooling can exceed 18 months.

This bottleneck is redefining competitive dynamics. Companies with in-house tooling capabilities and vertically integrated operations are gaining a decisive edge, securing long-term contracts with major beverage chains.

As a result, procurement strategies are evolving. Leading operators are entering joint-development agreements with manufacturers to guarantee access to production capacity, while also investing in secondary suppliers to reduce dependency risks.

Sustainability Meets Economics: The New Competitive Equation

The molded fiber packaging market is increasingly shaped by the intersection of sustainability and financial performance. Key drivers include:

Legislative Pressure: Global bans on single-use plastics are accelerating adoption.

Waste Economics: Rising landfill costs and composting incentives are favoring fiber solutions.

EPR Taxes: Packaging redesign is becoming essential to mitigate regulatory liabilities.

This convergence is pushing manufacturers to integrate sustainable packaging into broader product portfolios, enabling them to secure high-value, long-term contracts.

Competitive Landscape: A High-Barriers-to-Entry Market

The competitive environment remains highly concentrated, dominated by established players with advanced thermoforming capabilities and deep supply chain integration. Key companies include:

Huhtamaki Oyj

Pactiv Evergreen Inc.

Sabert Corporation

Sonoco Products Company

Genpak, LLC

Fabri-Kal

World Centric

U.S. Corrugated, Inc.

These companies are leveraging vertical integration from raw fiber sourcing to barrier coating technologies-to maintain quality consistency and protect margins.

New entrants face significant challenges, including high capital requirements, limited access to precision tooling, and the need to develop PFAS-free barrier technologies at scale.

For an in-depth analysis of evolving formulation trends and to access the complete strategic outlook for the Molded Fiber Lids and Cold-Drink Service Packaging Market through 2036, visit the official report page at: https://www.futuremarketinsights.com/reports/molded-fiber-lids-and-cold-drink-service-packaging-market

Explore More Research Reports by FMI

Foil Laminates Market - https://www.futuremarketinsights.com/reports/foil-laminates-market

Packaging Testing Services Market - https://www.futuremarketinsights.com/reports/packaging-testing-services-market

Composite Paper Cans Market - https://www.futuremarketinsights.com/reports/composite-paper-cans-market

Heavy Duty Bag and Sack Market - https://www.futuremarketinsights.com/reports/heavy-duty-bags-and-sacks-market

Track And Trace Packaging Market - https://www.futuremarketinsights.com/reports/track-and-trace-packaging-market

About Future Market Insights (FMI)

Future Market Insights (FMI) is a leading provider of market intelligence and consulting services, serving clients in over 150 countries. Headquartered in Delaware, USA, with a global delivery center in India and offices in the UK and UAE, FMI delivers actionable insights to businesses across industries including automotive, technology, consumer products, manufacturing, energy, and chemicals.

An ESOMAR-certified research organization, FMI provides custom and syndicated market reports and consulting services, supporting both Fortune 1,000 companies and SMEs. Its team of 300+ experienced analysts ensures credible, data-driven insights to help clients navigate global markets and identify growth opportunities.

For Press & Corporate Inquiries

Rahul Singh

AVP - Marketing and Growth Strategy

Future Market Insights, Inc.

+91 8600020075

For Sales - [email protected]

For Media - [email protected]

For web - https://www.futuremarketinsights.com/

SOURCE: Future Market Insights, Inc.